The feds are actually disturbingly fair about this. You can deduct your legal fees as a business expense.

wikipedia excerpt

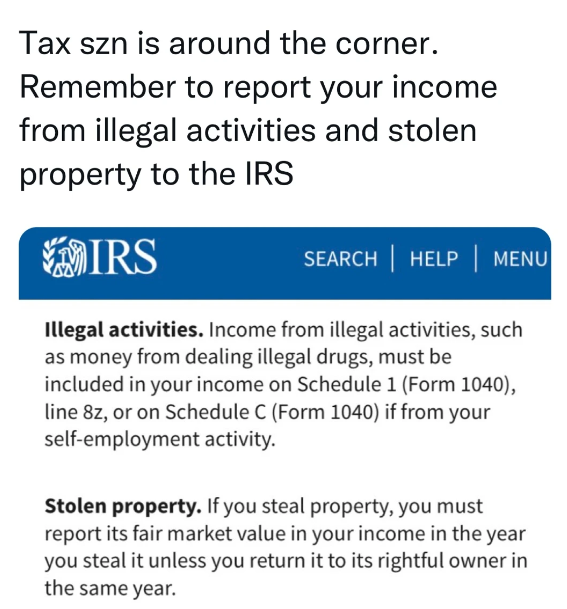

While embezzlers, thieves, and the like are forced to report their illegally acquired income for tax purposes, they may also take deductions for costs relating to criminal activity. For example, in Commissioner v. Tellier, a taxpayer was found guilty of engaging in business activities that violated the Securities Act of 1933.[8] The taxpayer subsequently deducted the legal fees he spent while defending himself.[8] The U.S. Supreme Court held that the taxpayer was allowed to deduct the legal fees from his gross income because they meet the requirements of §162(a),[9] which allows the taxpayer to deduct all the “ordinary and necessary expenses paid or incurred during the taxable year in carrying on a trade or business.”[10] The Court reasoned (and the Internal Revenue Service did not contest the point) that it was ordinary and necessary for a person engaged in a business to expect to have legal fees associated with that business, even though such things may only happen once in a lifetime.[9] Therefore, the taxpayer in Tellier was allowed to deduct his legal fees from his gross income, even though he incurred the fees because of his crime. The U.S. Supreme Court in Tellier reiterated that the purpose of the tax code was to tax net income, not punish unlawful behavior.[11] The Court suggested that if this was not the case, Congress would change the tax code to include special tax rules for illegal conduct

{kind=link}

The feds are actually disturbingly fair about this. You can deduct your legal fees as a business expense.

wikipedia excerpt

While embezzlers, thieves, and the like are forced to report their illegally acquired income for tax purposes, they may also take deductions for costs relating to criminal activity. For example, in Commissioner v. Tellier, a taxpayer was found guilty of engaging in business activities that violated the Securities Act of 1933.[8] The taxpayer subsequently deducted the legal fees he spent while defending himself.[8] The U.S. Supreme Court held that the taxpayer was allowed to deduct the legal fees from his gross income because they meet the requirements of §162(a),[9] which allows the taxpayer to deduct all the “ordinary and necessary expenses paid or incurred during the taxable year in carrying on a trade or business.”[10] The Court reasoned (and the Internal Revenue Service did not contest the point) that it was ordinary and necessary for a person engaged in a business to expect to have legal fees associated with that business, even though such things may only happen once in a lifetime.[9] Therefore, the taxpayer in Tellier was allowed to deduct his legal fees from his gross income, even though he incurred the fees because of his crime. The U.S. Supreme Court in Tellier reiterated that the purpose of the tax code was to tax net income, not punish unlawful behavior.[11] The Court suggested that if this was not the case, Congress would change the tax code to include special tax rules for illegal conduct